USD/JPY, Yen analysis

- FX intervention rhetoric shifts up a gear

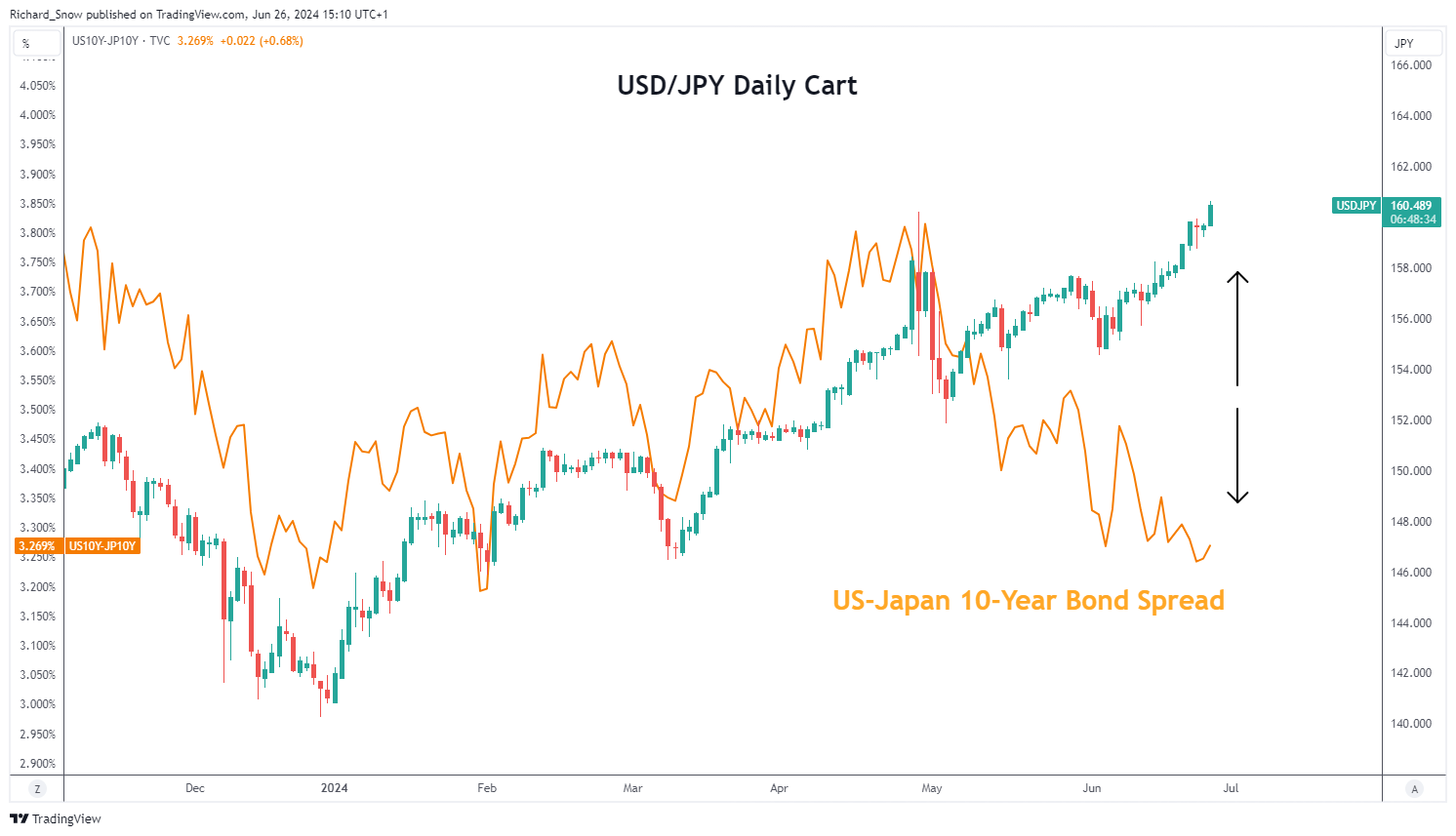

- USD/JPY completely ignores the decline in US-Japan bond spreads to trade higher

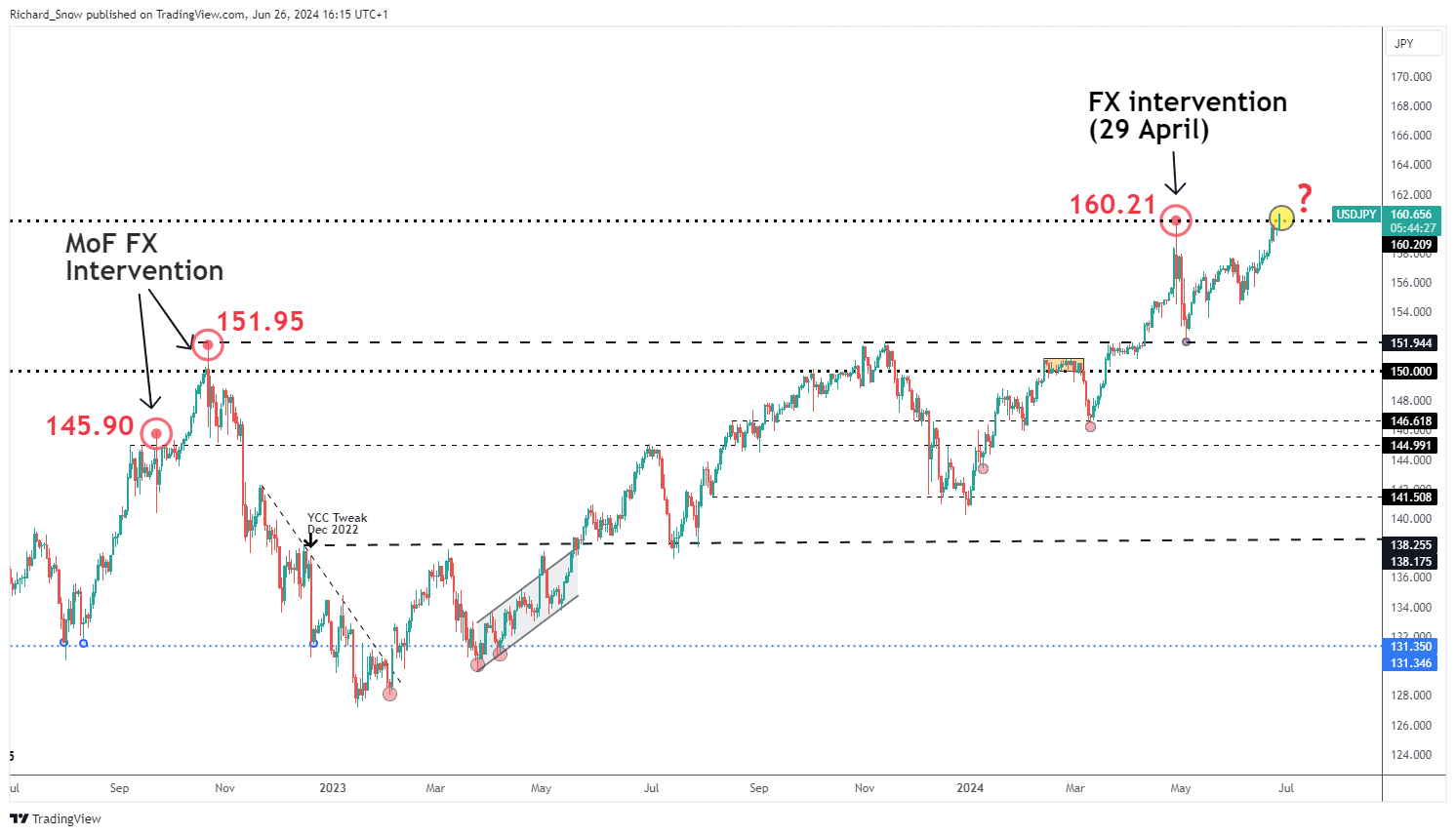

- The markets appear to be calling the Japanese officials’ bluff as every level of intervention has been surpassed since the 2022 interventions

- The analysis in this article uses chart patterns and key support and resistance levels. For more information visit our extensive education library

Recommended by Richard Snow

How to trade USD/JPY

Japan’s top currency official says yen’s recent weakness ‘not justified’

Japan’s chief currency official, Masato Kanda of the Ministry of Finance (MoF), has issued his sternest warning yet against unwanted, speculative moves in the currency world. However, markets appear happy to call his bluff as the USD/JPY has effortlessly surged past previous intervention levels.

Kanda indicated that he is deeply concerned about the yen’s recent rapid weakness, which is approaching the 4% gauge previously used to assess a “rapid” and undesirable decline in the currency. Before the FX intervention in April, Kanda clarified that a 4% depreciation over a two-week period or a 10% decline over a month meets the definition. Since the swing low in May, the yen had depreciated by about 3.15% in two weeks, which is close to the 4% rule of thumb.

At the time of writing, USD/JPY recorded an intraday high (the London session) of around 160.81, reaching oversold territory on the RSI.

USD/JPY daily chart

Source: TradingView, prepared by Richard Snow

USD/JPY completely ignores the decline in US-Japan bond spreads

Recent developments in Japan have caused Japanese government bonds to rise above 1% again, but USD/JPY found no relief and still traded around and above 160.00. The US-Japan bond spread typically guides USD/JPY, as seen below, but the pair appears to have broken away from the yield differential.

The BoJ did not provide details of a long-awaited reduction of its bond portfolio at its latest meeting. There she previously spoke about reducing purchases that have kept Tokyo’s financing costs low. However, the BoJ stated that this will be available at the end of next month at the July meeting.

In the meantime, Friday could provide insight into the Bank’s appetite for bond-buying, when the BoJ is expected to release its new bond-buying schedule. A combination of a shorter bond purchasing schedule coupled with a potentially lower US PCE figure could provide some respite for USD/JPY heading into the weekend, but that seems a tough ask given the recent reluctance to to stop the increase.

Recent break between USD/JPY and US-Japan 10-year bond spreads (orange)

Source: TradingView, prepared by Richard Snow

A dangerous game of bluffing: markets versus the Ministry of Finance

Markets appear to be calling the Treasury Department’s bluff, trading comfortably above 160.00 – the latest level that prompted officials to sell tens of millions of dollars to finance massive purchases of the yen. Whatever happens, this remains a pair with excessive potential volatility that can occur without warning – underscoring the importance of sensible risk management. Previous intervention efforts produced moves around 500 pips.

Previous, surpassed cases of currency intervention

Source: TradingView, compiled by Richard Snow

— Written by Richard Snow for DailyFX.com

Contact and follow Richard on Twitter: @RichardSnowFX