By means of Dearbail Jordan and Faisal Islam, Business reporter and economics editor

Getty Images

Getty ImagesThe Bank of England opened the door to a rate cut in August, which would be the first fall in borrowing costs in more than four years.

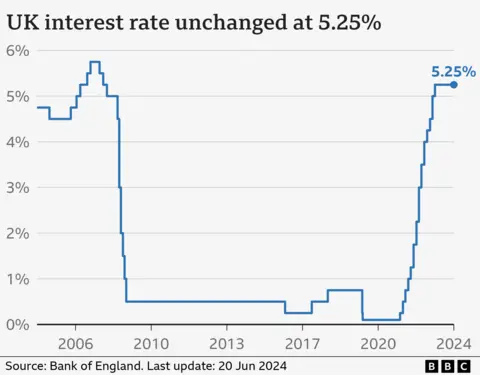

In a close-run decision on Thursday, the Bank voted to keep interest rates at a 16-year high of 5.25%.

Earlier this week, Figures showed that inflation – which measures the pace of price increases – had fallen to 2% in May, in line with the Bank of England’s target. However, prices of some items continued to rise faster than expected.

But the minutes of the Bank’s rate-setting committee indicated a significant change in tone, suggesting a majority could vote for a cut when they meet again on August 1.

They say they will watch to see if the areas of concern “retreat.”

“Based on this, the committee will determine for how long [the] Bank interest rates should be maintained at current levels,” the minutes said.

While not a foregone conclusion, this language is a clear signal to the markets and the public that, after the Bank finalizes its new forecasts for the economy, a rate cut is now the most likely outcome at its next meeting.

The rate-setting committee voted 7-2 to maintain rates, but the outcome was not as dry as before. For three members, the vote to hold this month was a “balanced” decision.

The committee members leaning towards austerity, which also includes Bank of England Governor Andrew Bailey, are downplaying the strength of underlying inflationary pressures.

The Bank’s latest decision comes in the run-up to the general election, with policies for the future of the UK economy a key battleground for political parties.

However, the Bank stressed that the timing of the elections was “not relevant to its decision”.

Bank of England interest rates are having a knock-on effect on mortgage, credit card and savings rates for millions of people in the UK.

Although the Bank appears to be hinting at a cut in August, many homeowners now coming to the end of a fixed rate agreement are facing mortgage rates that are much higher than they are used to.

The current average rate for a two-year fixed deal is 5.96%, although this is down from last year’s peak of 6.86%.

People in tears over mortgage payments

Ben Perks

Ben PerksMortgage adviser Ben Perks, who works in Wolverhampton, told BBC Radio 5Live that while he was not surprised by the Bank’s decision to keep rates on hold for the time being, he was “definitely disappointed and certainly frustrated”.

“It’s fine to say, ‘Oh, we’ll wait’, but the reality is that 125,000 people a month are coming to the end of their flat rate, which over a two-month period is the population of Wolverhampton city center .”

He says he has had borrowers in his office in tears when they found out how much their mortgage payments would increase.

“It’s extremely stressful. We’ve had meetings when you told them the new payments and because everything else has gone up, they don’t know which way to go.”

Wednesday’s inflation data showed that price increases for services – which reflect the cost of things like movie tickets, restaurant meals and vacations – remained higher than expected.

But the Bank’s minutes show that the slow decline in services inflation reflects one-off factors, including the rise in the minimum wage and bills that automatically rise with inflation, such as broadband and mobile.

If the Bank goes ahead with a rate cut in August, it would be the first since March 2020, when Britain was heading into its first Covid lockdown.

“It is good news that inflation has returned to our target of 2%,” said Bank Governor Andrew Bailey.

“We need to be sure that inflation will remain low and that is why we have decided to keep interest rates at 5.25% for the time being.”

The Bank of England is independent of the government and its main role is to keep inflation stable at 2%.

In response to high inflation, the Bank has raised interest rates in recent years and subsequently kept them at a high level.

The theory behind rising interest rates is that this will slow inflation, but it could also slow economic growth because companies may delay investments or hiring, which could mean fewer jobs are created.