Official opinion polls suggest Britain is on course for a change of government next week after 14 years of Conservative Party rule, with the new leadership tasked with pulling the economy out of the doldrums.

Labour looks set for a historic victory, with Keir Starmer’s party pledging to deliver the highest sustainable economic growth in the G7 “with good jobs and productivity growth” as Britain transforms into a “clean energy superpower”.

But whoever wins on July 4, it will do so in the shadow of Liz Truss’s disastrous 2022 mini-budget and the havoc that unfunded tax cuts have wrought on the country’s finances – and on the personal finances of its citizens.

So how will debt markets react to a change of government and can Britain revive its economic fortunes while avoiding another market crisis?

Labour Party leader Sir Keir Starmer and Shadow Chancellor Rachel Reeves are keen to emphasise fiscal responsibility in the party’s manifesto.

Gilts in fashion

Retail investors have been flocking to government bonds (UK government-issued debt) since the start of the year, attracted by solid returns and an expectation of a rise in bond values as interest rates begin to fall later this year.

Hargreaves Lansdown said in April that first-quarter government bond purchases on its platform were three times higher than the same period last year, while Interactive Investor saw its best month for government bond sales in ten months.

The interest of private investors is mainly focused on government bonds with a short term, which mature within a few years. There is more clarity about the direction of interest rates and the time horizon for them to get back the full value of their investment is shorter.

Demand for the bonds has increased now that the base rate has peaked and the first interest rate cuts from the Bank of England are in sight.

The price of a bond rises and falls inversely with its yield. The yield on two- and five-year government bonds has fallen by 91 and 52 basis points respectively in the past year.

Now that two- and five-year yields are at 4.2 and 4 percent respectively, they are well below their post-Truss peak.

Analysts say the UK has done a good job restoring bond investor confidence after the Liz Truss market crisis in late 2022

Manifestos were received with a shrug

Unlike the Truss era, when developments in Westminster angered bond watchdogs, markets have hardly bothered about the release of party manifestos ahead of the general election.

Yields on two- and five-year bonds have fallen by 27 and 16 basis points respectively over the past month, while longer-term yields have also fallen.

However, analysts say this is due to the expectation of impending interest rate cuts, and not due to political promises.

Susannah Streeter, head of money and markets at Hargreaves Lansdown, said: “So far, the commitments and promises made do not appear to have disrupted debt markets, with yields on 10-year and 30-year UK government bonds falling back on the previous week, [and] Bond investors appear to be more sensitive to interest rate speculation than to the investment plans of a new government.’

Politicians, they are all the same!

But the absence of an overtly negative response to the Tory or Labor manifestos can be at least partly attributed to each party’s reluctance to the generosity of their respective pledges.

The Conservative government and Rachel Reeves, Labour’s shadow chancellor, have both committed to so-called ‘fiscal rules’, which require the debt burden as a share of GDP to be on track to fall within a five-year parliamentary term.

Due to the teetering and ever-growing debt mountain that our governments have built up over the past thirty years, we do not have the financial leeway for ‘out of the box’ policies

Fredrik Repton, senior portfolio manager at fund house Neuberger Berman, said both current Chancellor Jeremy Hunt and the BoE had done a “good job” of restoring investor confidence in Britain through tighter policy and effective market communications.

Both parties do not want to damage this trust.

Tom Becket, co-chief investment officer at Canaccord Genuity Wealth Management, said: ‘Given the looming and ever-increasing debt mountain our governments have built up over the past 30 years, we don’t have the financial or fiscal space for out-of-the-box policies.

‘Fortunately, the Labor manifesto seems quite stable. The hapless Liz Truss government was a stark reminder of the practicalities of overseeing our country in its precarious financial position.”

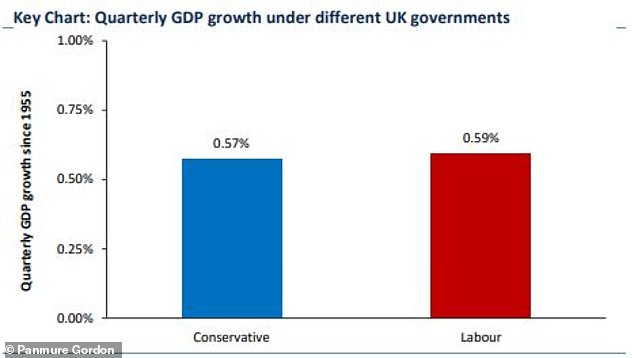

Comparison of the economic growth performances of previous Labour and Tory governments

A ‘changed’ Labor Party and its crucial first budget

As part of efforts to demonstrate Labour’s renewed commitment to fiscal responsibility, Reeves has dropped a £28 billion-a-year green investment plan that formed the basis of the Labour Party’s offer to the British public just a few months ago.

Nor have Reeves and Starmer made any attempt to hide their efforts to warm to the City, with Labour keen in the eyes of the markets to shake off its Corbynite recent past.

Neuberger Berman’s Repton told This is Money that there are currently no major differences between Britain’s two largest parties in the debt markets.

He said: ‘That’s why we see markets being so optimistic about the elections.

‘We manage bond funds, we are not political analysts. But when we look at this, we don’t see any material difference, at least at first glance.

“We expect the Labor Party will also be fairly conservative in the way it communicates with the markets.”

The pound sterling has performed worst against the dollar when Labour was in power

However, Repton warned: ‘There is always the risk that discipline may deteriorate somewhat over time’ and Labour’s first budget ‘will be very important’.

While both Labour and the Tories have been keen to talk about their own fiscal responsibility, they have also been noticeably vague about their tax plans.

Both parties have ruled out increases in the state’s main sources of revenue – income tax, national insurance and VAT – while denying they will make increases elsewhere.

This is despite the fact that most economists agree that tax revenues will need to increase in the next parliamentary term, even to meet current spending and debt service obligations.

Repton said: ‘This is something that has to be addressed at some point, regardless of who wins the general election.’

Does the color of the rosette actually matter?

Research from investment platform eToro shows that 44 percent of retail investors believe a Labor victory in the general election will be a bullish sign for UK stock markets, while 30 percent say the opposite.

Canaccord GWM’s Becket said international investors could “breathe a sigh of relief because of the change of political guard” after a period of stagnation in Britain.

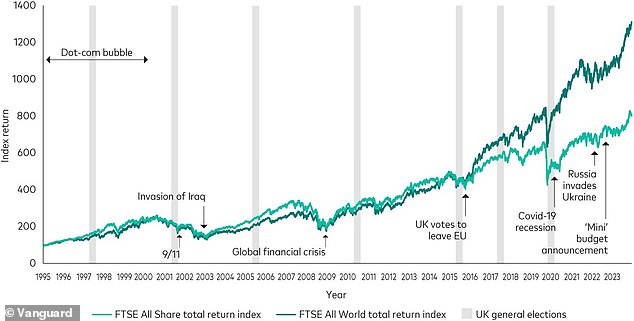

But analysis by fund giant Vanguard shows that the UK stock market has been largely unaffected by the election in recent times.

Vanguard data shows that the seven general elections that took place between January 1995 and December 2023 had “minimal impact on stock market performance.”

It added: ‘The events that most affected the stock market were on a much larger, global scale.

‘These included the bursting of the dot-com bubble (when technology stocks fell after a rapid rise in valuations in the late 1990s), the global financial crisis in 2007-2009, and the Covid-19 pandemic in 2020.’

Vanguard data shows that the general election had little impact on the outlook for UK shares overall

And longer-term analysis by Simon French, chief economist and head of research at Panmure Gordon, suggests the policy difference between Labor and the Tories is not as stark as many voters might think.

French said: ‘The quarterly GDP figures of the Conservative and Labour governments are virtually identical.

‘There is no historical evidence – at least since reliable GDP data became available – that Conservative or Labor governments are better or worse for growth in the UK economy.

There is no historical evidence – at least since reliable GDP data became available – that Conservative or Labor governments are better or worse for growth in the UK economy

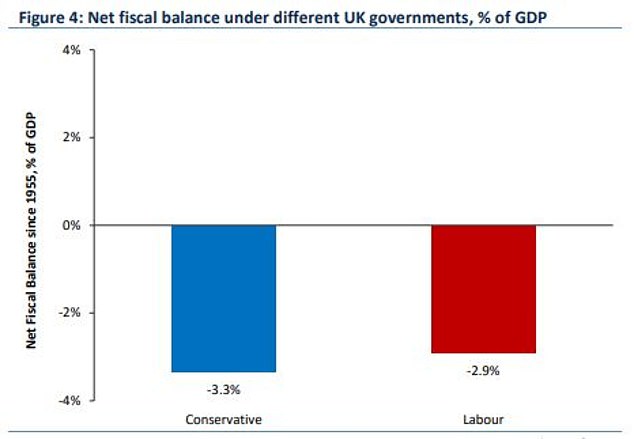

‘In terms of fiscal policy, this is probably the finding that most contradicts the prevailing commentary/conventional wisdom. Since 1955, budget deficits under Labour governments have been modestly smaller (2.9 per cent of GDP) compared to Conservative governments (3.3 per cent of GDP).

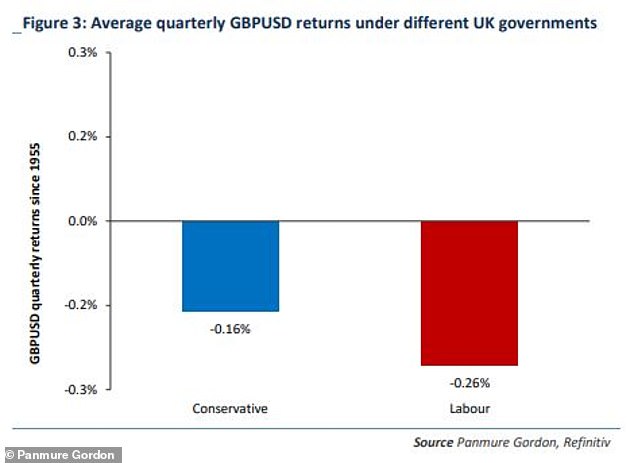

‘Another aspect that capital market participants need to consider is the strength of the pound under different governments.

‘On average, the long-term weakening of GBPUSD over the past 70 years has been greater under Labour governments (-0.26 percent quarter-on-quarter) than under Conservative governments (-0.16 percent quarter-on-quarter).

“These are relatively small differences, however, and it is difficult to identify a pronounced difference in currency performance amid a general devaluation trend.”

Since 1955, budget deficits under Labour governments have been slightly smaller than under Conservative governments.

Some links in this article may be affiliate links. If you click on them, we may earn a small commission. That helps us fund This Is Money and keep it free to use. We do not write articles to promote products. We do not allow a commercial relationship to affect our editorial independence.