By means of Michael Ras, Business reporter, BBC News

Getty Images

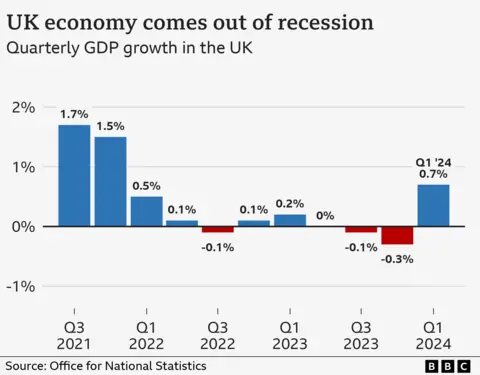

Getty ImagesThe economy grew stronger than initially expected in the first three months of 2024 as Britain emerged from recession, revised official figures show.

The economy grew by 0.7% between January and March, the Office for National Statistics (ONS) said.

Growth was initially estimated at 0.6%, according to figures released last month.

The strength of the economy was a central battleground in the election campaign, with growth having been sluggish in recent years.

Most economists, politicians and businesses want GDP to rise steadily. This means that people spend more, more jobs are created, more taxes are paid to the government and employees receive a better salary.

The original figure for the first quarter of the year was higher than economists had expected, as growth in the services sector, which includes businesses such as hairdressers, banks and hotels, led to an increase, the ONS said.

But while service sector growth was revised upward, manufacturing growth was revised downward as more data was collected.

The upward revision made the UK the fastest-growing economy in the G7 group of advanced economies in the first three months of this year.

Prime Minister and Conservative leader Rishi Sunak welcomed the new revised growth, saying his party had a “clear plan to deliver a more secure future for your family”.

But Sarah Olney, spokesperson for the Liberal Democrat Treasury, said despite the upward revision, the figures would be “cold comfort to families hit by rising mortgage repayments, unfair stealth taxes and the soaring cost of a weekly grocery shop”.

The Labour Party has not commented on the latest statistics.

Paul Dales, chief Britain economist at research firm Capital Economics, said faster GDP growth in early 2024 was “mainly due to upward revisions in consumer spending”.

The ONS said there was more spending on leisure and culture, as well as housing and food, but household disposable incomes continued to rise in early 2024 as workers secured pay rises.

According to Mr Dales, this means that the household savings rate has risen from 10.2% at the end of last year to 11.1%. This is the highest percentage since mid-2021, when the savings rate was increased during the Covid pandemic.

He added that the new figure suggested that “whoever is Prime Minister this time next week could benefit from the economic recovery being slightly stronger”.

“It’s only a small improvement, but when it comes to UK GDP growth, every little bit really helps,” said Danni Hewson, head of financial analysis at AJ Bell.

“Growth is central to party manifestos, even if they differ on the details of how that growth can be achieved. A growing economy creates prosperity, puts more money in people’s pockets and increases the amount of taxes going into depleted coffers. “

Although Britain has emerged from the economic recession of the final months of 2023, many households may not feel better off as budgets have been stretched recently by rising prices.

Interest rates are currently at a 16-year high of 5.25%. This means people are paying more to borrow money for things like mortgages and loans, although savers have also received better returns.

The latest figures on the economy show it failed to grow in April after particularly wet weather put off shoppers and slowed construction.

The Bank of England, which sets interest rates, has opened the door to cutting them in August, which would be the first fall in borrowing costs in more than four years.

But many mortgage holders have already refinanced their mortgages at a higher cost, and approx Another three million households will see their repayments increase over the next two years as fixed interest rates expire.

Sophie Lund-Yates, chief equity analyst at Hargreaves Lansdown, said that while “hotter-than-expected growth doesn’t help those looking for a quicker route to rate cuts, it does boost overall optimism”.

“The UK’s entrenched productivity problems are, overall, a bigger concern than the immediate interest rate outlook,” she added.