A wave of speculation by traders in futures markets has pushed the prices of metals such as copper and gold to record highs, as funds bet on coming supply shortages and try to hedge against inflation.

Copper has risen 30 percent since early March and this week broke through $11,000 per tonne, its highest level ever. That has helped push up prices of other industrial metals from aluminum to zinc.

The rush of investor buying also pushed gold past its previous records to reach $2,450 per troy ounce, with silver above $30 per ounce for the first time in a decade.

There has been “strong investment” in metals from algorithmic traders, specialist commodity investors and macro funds, said Greg Shearer, head of base and precious metals strategy at JPMorgan.

The moves in metal prices have often defied traders’ expectations. Last year, strong demand helped push inventories to historic lows, but prices still fell. This year, prices have risen, even as supply improves.

Meanwhile, according to data from Bloomberg, the share of commodities in global markets has fallen from 8.8 percent in 2009 to 2 percent in the past 12 months, while stocks and bonds have soared.

“The market ignored everything from a fundamental perspective,” said Ricardo Leiman, chief investment officer at KLI Asset Management, a London-based commodity investment manager.

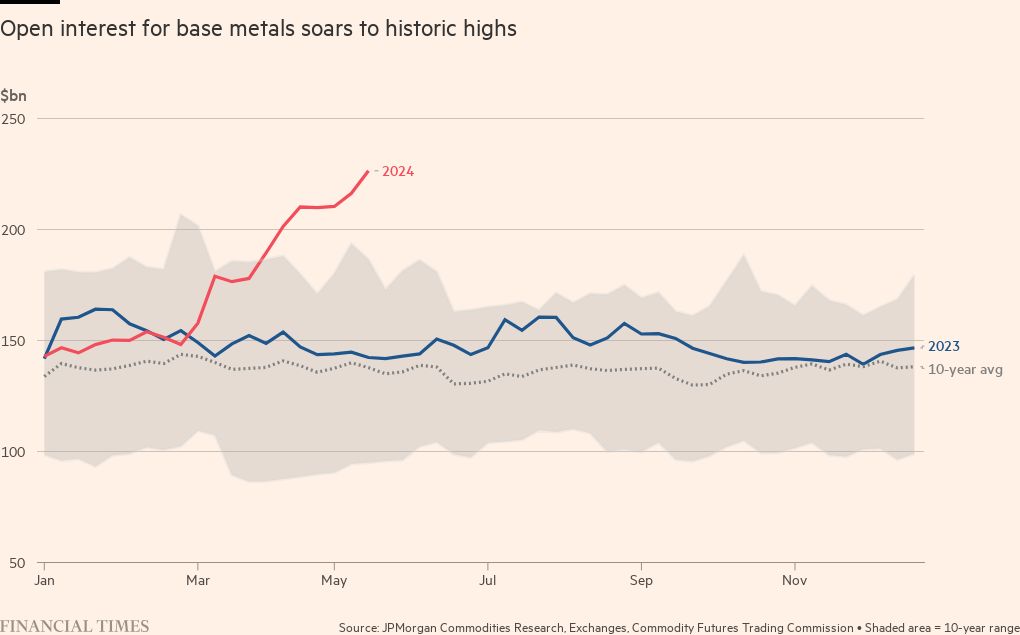

Analysts said these moves were driven by a rise in open interest – the number of open futures positions and the depth of the market.

Open interest in the base metals and precious metals markets reached record highs last week of $227 billion and $215 billion, respectively, according to a JPMorgan analysis.

This largely consists of funds that make their bets on falling prices and funds that take long positions to profit from price movements, rather than producers or consumers hedging against the risk of price movements when buying or selling commodities, analysts said.

Investors’ net long positions on Comex and the London Metal Exchange for base metals stood at 2.6 million tonnes in mid-May, up from 556,000 tonnes in early March, surpassing the previous high at the end of 2020.

The wave of money hitting the metals is coming not just from momentum-driven algorithmic traders, but also from macro hedge funds that have increased their allocation to real assets and specialty commodity hedge funds, analysts said.

Copper, which is critical to the decarbonization process, has led the price increases. Shearer said a “very difficult to correct supply picture” was supporting copper’s rally.

“For copper, the tighter supply is one times as large as possible [artificial intelligence] A surge in demand and greater certainty that we are at an inflection point for global demand, plus hedging inflation, has been a powerful brew,” he said. “That has caused many funds to say: ‘now is the time for copper’.”

Other base metals such as zinc, aluminum and lead followed copper, rising between 15 percent and 28 percent in a sharp collective increase since early April.

Aline Carnizelo, managing partner of Frontier Commodities, a newly formed commodities investment vehicle, said investors were looking to diversify their returns away from big tech stocks by focusing on metals.

Funds are putting money behind commodities to gain exposure to “decarbonization, deglobalization, a hedge against inflation and geopolitical risks, as well as the underinvestment in new supplies, especially of energy,” she said.

Inflows into broad-spectrum commodity funds – including grains, minerals, metals, cotton and cocoa – have risen in recent months and more than doubled in April to £1.9 billion, according to Morningstar data.

Despite weaker-than-expected demand in China and a rapid build-up of metal inventories, there are signs that global manufacturing is finally turning around, which has also contributed to interest in silver given its extensive use in solar panels. The Chinese purchasing managers index rose for the second month in a row in April, after six months of contraction.

Australian mining group BHP’s £34 billion move to buy rival Anglo American to secure its coveted copper mines in Latin America also sent a signal to investors to get their hands on the red metal.

“The BHP acquisition has woken up a lot of people to the fact that it is much cheaper to buy a company than to build a new mine,” Leiman said. “It caused a lot of people to unwind their positions [computer-driven trend-following hedge funds] and part of the macro crowd goes long. There has been a huge reorganization of flows.”

A net of 13 percent of global fund managers surveyed by Bank of America were overweight commodities in May, the highest since April last year. According to the research, the past three months saw the largest increase in their commodity allocation since August 2020.

Some top hedge funds have expanded their commodity trading teams to take advantage of volatility in the asset class. Family office BlueCrest Capital plans to expand the number of trading teams, including in commodities, by 10 percent by the end of the year.

Commodities are typically traded based on their current supply and demand situation, but Carnizelo said the increasing role of speculative investors in the market means they are starting to trade based on the likely picture of the future.

“It’s starting to make commodities behave a bit like stocks,” she said.